Are the hard data beginning to reflect Trumpian chaos?

Economic numbers sometimes take time to catch up to consumer vibes.

For years, first as a member and then as chair of President Joe Biden’s Council of Economic Advisers, I had a ringside seat to the great data/vibes split. Starting in 2022, inflation begin to come down quickly, while growth and jobs remained strong. But most people were too unhappy with the higher price level to feel good about whatever else was going on in the economy.

Under President Donald Trump, that gap has not only remained in place, but it has gotten larger. By most measures, the economy is still good according to most of the so-called “hard” data (meaning inflation, jobs, and growth as opposed to consumer and business sentiment, aka “soft” data).

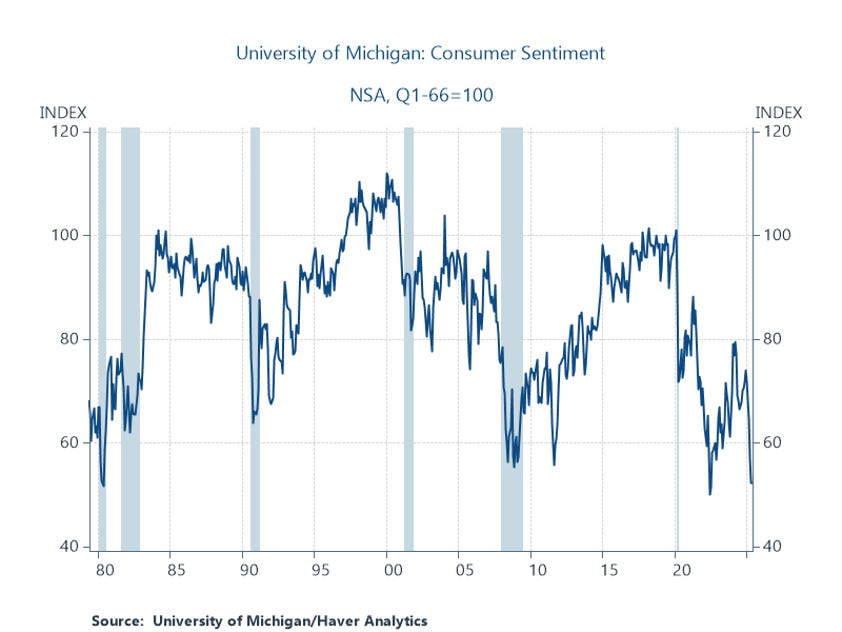

There’s a good explanation for this. First, much of the soft data show that Trump’s trade war, DOGE cuts, disregard for rule of law, and all the rest of the chaos are working everybody’s last good nerve. The figure below shows the recent cliff dive of consumer sentiment, which is down to historically low levels. In fact, you rarely see a decline of this magnitude outside of recessions (the shaded parts).

Now, before we go on, an important reminder: This post is all about data, and data are noisy, especially in periods like the present, with so much policy upheaval. A different confidence survey, the one by the Conference Board, saw a spike up in May, though that same group found the CEO confidence is tanking, posting “the largest quarter-over-quarter decline in the history of the survey, which started in 1976.” I, therefore, will be careful throughout to cite caveats as to what might be a blip and what looks more like a potential trend. And, in this case, I’m very confident in asserting that Trump’s economic agenda is hurting consumer, business, and market confidence.

The second reason for the widening data/vibe gap is that it can take months for the data to reflect even consequential policy changes. This is a big, $30 trillion, globalized economy, and absent shocks like the pandemic, it rarely turns on a dime. This time delay is exacerbated by the on-again-off-again nature of the trade war.

But the fact is we’re starting to see in the hard data some clear--—and some less clear--—impacts of Trump’s recklessness. With caveats as to what’s a potential trend and what’s a data point on which we shouldn’t over-torque, here’s what I’m seeing:

· The most obvious response in the hard data to the trade war is tariff-frontrunning by American businesses racing to get the imports they need here before the import taxes take effect. Imports are a subtraction from GDP—we must net out foreign purchases in order to calculate domestic production—and their huge negative spike in 2025Q1 led real GDP to contract slightly, by 0.2%.

· We just learned that in April imports reversed course; after growing by $53 billion through March of this year (up 18%, a historically large jump), they fell back by $66 billion in April, down 19%, the largest monthly decline on record for this series.

· These distortions made Q1 look worse than it was and will make Q2 look better, but they clearly reveal the extent to which the trade war is messing with the data.

· In a potentially worrisome development, real consumer spending slowed in Q1 and in April as well. It came in at 1.2% in the quarter, down from 4% in the prior quarter, the lowest rate in almost two years. April’s real spending also came in weak, up just 0.1% for the month.

· However, these are data points, not trends yet, and it’s not at all uncommon for a weak month to be followed by a stronger one. Moreover, the American consumer has, for years now, relentlessly driven this economy forward. Spending is almost 70% of our GDP, and pandemic-era fiscal support followed by strong compensation from the full-employment labor market has long fueled this growth source.

· Which brings us to the labor market, probably the most important sector of the economy that has yet to show much weakness at all. The unemployment rate is 4.2%, up from 3.9% a year ago, but still pretty low. And job growth has been solid, averaging about 150,000 per month over the past three months.

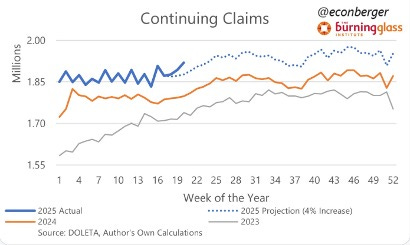

· That said, there’s one last hard data point that has moved up on my watchlist: so-called “continuing claims” for the Unemployment Insurance program, meaning the number of people stuck on unemployment insurance versus the weekly inflow (aka, initial claims). The figure below, from Guy Berger, research director at the Burning Glass Institute, reveals these claims to be a bit elevated (see “2025 Actual” line), leading Berger to tweet: “Continuing claims really does look like a modest deterioration relative to benchmark - this week's print was about 32K above it.”

These elevated claims reflect the fact that the rate of hiring has slowed such that it’s taking longer for people to leave unemployment for their next job. That’s not great, but slower hiring is not equal to higher layoffs, and, absent a spike in layoffs, we should conclude that the job market is still in decent shape.

But, with all those caveats and messy data going this way and that, there’s enough here to worry about. I didn’t mention inflation as it has been benign, but there’s that lag effect I noted above. There is a high likelihood that, thanks to the tariffs, higher prices are coming. And, most important, if it turns out that the job market and consumer spending are weakening, then we have a real problem on our hands.

Either way, every data watcher, including me, will be carefully scrutinizing these next few weeks of data reports, starting with the May jobs report out this Friday. My profound hope is that the negative data points noted above are head fakes, not new trends. But actions have consequences, and that goes for the most reckless economic agenda we’ve ever seen.

So, stay tuned and fasten your seatbelts. It’s going to be a bumpy ride.

Jared Bernstein was chair of President Joe Biden’s Council of Economic Advisers.

Not reflected in the employment data, but definitely happening is the fact that it is much harder for professionals in a variety of fields to get new jobs. Just in my limited experience, I see a nonprofit manager, a digital marketing expert, a user experience expert, and a technical writer getting nowhere in job searches. I'm not sure why this is occurring, but it has to have at least some relation to the chaos in the economy and country in general. And what are all the discharged federal employees doing other than getting unemployment??

I'll be waiting to see what happens. As Mr. Bernstein writes "it can take months for the data to reflect even consequential policy changes".